Anyway, Alan has really done his home work on this one. He discusses the marginal tax rate that some oldsters face; a marginal rate more than 100%. That's right, they pay more in taxes than they get for working!

This is his commentary.

Alan Mole/ 1441 Mariposa Ave. /Boulder, CO 80302/ r a m o l e@aol.com/ (303) 440-7385

August 4, 2010

Returning Workers Can Save the Country

There is a way to save Social Security and pay the National Debt. It is painless, voluntary, and a win-win game for everyone involved. The method is simply to recognize the value of older workers and encourage them to continue working, but only for as many hours as they like. Yet that simple change can save the country.

Few people realize the value of an older worker to the Treasury. Sure, Bill knows metal forming better than any kid, and Jane is the best librarian we ever had, but why do their taxes in particular count for so much?

Their taxes count extra because they are pure gravy. Their Social Security contribution causes no increase in their payments, their Medicare taxes don't buy them anything extra, and their income taxes are an unexpected gift. They are a boon to their country.

Let's be specific. The cases for Medicare and Income Tax are clearest.

If Bill, a retiree, returns to work, he and his employer combined pay 2.9% for Medicare tax, but he gets no added benefits. None at all, no matter what. Not one extra aspirin. If Bill earns $40,000, Medicare gets $1160.

Most important, Bill pays income tax. Absolutely pure gravy for the government, which expected him to be retired and earning nothing. Besides which, Bill is already educated and trained, so there is no investment required, no job training, nothing at all. His taxes are unencumbered, an unexpected gift. At a 25% combined rate for Federal and State tax, Bill pays $10,000.

These two additions to the wealth of the Treasury are the most important and clearest, while Social Security is a bit more complicated, so any reader wishing to stop here and jump to Actual Numbers should please feel free.

For Social Security the rules are so complicated they are hard to understand, but the benefits are real. Bill and his employer pay 6.4% each, so on $40,000 SS makes $5120. Yet Bill's monthly benefits do not increase, except in a few cases where they rise slightly, but nowhere near what they would for a younger worker. Social Security really profits on “Bills”. (See details on next page.)

Actual Numbers

How much can these taxes add up?

If Bill returns to work, earning $40,000 per year, then as seen above, over $5000 per year goes to Social Security. Today there are 36 million Americans over 65 and by 2050 there will be 87 million. Let's take 70 million as a reasonable average. If we can persuade just 10% of them to go

Social Security Details

First, let's dismiss an irrelevant rule that makes the government just break even. If you delay Social Security from 66 to 67, then it pays you 8% more per year. The government saves one year of payments, and uses this money plus the interest on it to pay you about a 12th more yearly for the remaining 17 years of your life expectancy. This is break-even, so we can forget it. And it is break-even whether you work or not.

The important question is, If you work, does your base amount increase? Only rarely, and then not by very much. (Your base amount is the monthly payment you receive if you retire at the full retirement age (now 66) and are single. Everything else is calculated from this.) Base amount is calculated on your best 35 years of earnings (as adjusted for rising salaries.) But at 66 a worker already has 45 years of earnings. If he has always been a clerk or assembly line worker, all his years' adjusted earnings are about the same and he already has ten years' extra wages, so an eleventh extra year will not affect calculations. If he works only three-quarters time after 66, taking three extra months' vacation to travel, he will make only three-quarters of average earnings, and that certainly won't displace any other year, so there will be no change in his payments. This will be the case in most instances. The exception is complicated, so again if you want to skip ahead...

If Bill makes a lot more at 66 than in some previous year among his best 35 years, then his 66 earnings displace those of the other year, and his base amount increases a little. Suppose Bill has been promoted to manager, and this year's earnings of $50,000 exceed a year of $30,000 in his top 35 years. Then only the difference enters the calculation: $50,000-$30,000 = $20,000. So $20,000 goes into the calculation, yet he has paid Social Security on all $50,000. The government still makes out. And, that $20,000 is divided by 420 months ( 35 years) and added to his average adjusted monthly salary. The first part of that average, $656, is multiplied by 0.9 to give him a $590 portion of his base amount. The .9 factor is a very generous gift to the poor. The next $3299 is multiplied only by 0.32, and if he has all of that it yields $1055 more. Anything above that is multiplied only by 0.15. In other words, so as to be generous to the poor the first $656 is overpaid, and to get the money for that, anything over a total of $3955 is underpaid.

Why is this important? Because most people of middle income are already in that 15% bracket for their top dollars, so even if they do earn enough to displace another year, only the difference between years gets counted and even that is multiplied only by a small percentage -- 15% probably, 32% at most.

So Bill pays full Social Security tax on all his earnings, and probably gets no increase in return. Or only a very small increase.

back that's 7 million workers, and 7 million x $5,000 = $35 billion a year, or $1.75 trillion over 50 years.

Medicare will get $1120 from Bill's employment, and at that rate 7 million extra workers will pay almost $8 billion a year, or $0.4 trillion over 50 years.

Bill's income tax will be about 25% of $40,000 = $10,000. For 7 million workers over 50 years that's $3.5 trillion.

But wait there's more! Yes, it gets better still. Remember the theory that a dollar goes around seven times? A military base is built in a poor community, bringing a substantial payroll. But each dollar raises community income by $7, so each single soldier supports seven jobs. How? Well the soldier spends a dollar with the grocer, who spends the dollar at the butcher's, who spends it at the barber's, and so on. On average it passes through seven hands before being spent outside the community and vanishing. This is called the multiplier effect.

The added earnings of the un-retired work the same way. They increase wealth seven times as much, which increases taxes by seven times what Bill pays. This means we can solve all our problems with money left over.

The National Debt is nearly $10 trillion. But seven times "Bill's" Income Taxes over 50 years is $25 trillion. We can pay off the debt with $15 trillion left over. (Note: This was written last year, and it is very hard to keep current on the National Debt. Yes, it is more now.)

Social Security will owe $2 trillion more than it takes in over the next 50 years. But seven times the extra contributions for 50 years is $12 trillion, a surplus of $10 trillion.

Medicare is the most frightful problem, dwarfing the other two with a horrible $30 trillion shortfall over 75 years. (But since all the other figures are for 50 years, let's prorate that to $20 trillion over that time period. Then we can compare like with like.) In 50 years "Bill" will pay $.4 trillion in extra Medicare taxes. Seven times $.4 trillion is only $2.8 trillion, not nearly enough. But add in the two surpluses above and we have $28 trillion, enough to pay Medicare with $8 trillion left over! We can fix it all!

Just 10% more retirees working will painlessly save the country. Does the government realize this? Does it appreciate what a salvation older workers are? Not apparently, because it does so much that discourages their work.

Triple Taxation for Older Workers

Congress understands the Laffer Curve and has adjusted ordinary tax rates to take it into account. Prof. Laffer said a marginal tax rate over 40% was counterproductive. Less money came in than with a lower rate, because above 40% people spent more effort avoiding taxes than in making money, or they grew so disgusted they threw down their tools and went fishing. This is why Ronald Reagan got the federal tax rate reduced. It was a good idea, which stimulated the economy and induced wonderful economic growth. Yet when it came to older workers, Congress utterly ignored the lesson. It passed laws that can raise effective tax rates to 103%. Yes, that's right, an older worker may lose so much to the government that he is several cents poorer for every dollar he earns! No wonder so many people quit.

Note: The rates and limits used below change slightly each year for inflation.

One may earn up to $13,000 at low tax rates, but above this it gets discouraging. So most workers stop at around one-quarter time. And, if they can’t arrenge for quarter time they probably don’t work at all, or take a job below their training (usually referred to as “Walmart greeter”.)

Here's how the effective rates get so high. If your total income, including half your SS, is less than $25,000 (single), then SS is not taxed at all, but for every dollar over that, 50-85¢ of a dollar of SS is taxed. And for every dollar you earn over $12,480 your SS payment is reduced 50¢ (ages 62-67 only). Thus Jane may be in a position where she earns $1, but she is taxed on $1.85 (the dollar she earned plus 85¢ of an SS dollar). If she is in a marginal tax bracket of 25% (Federal plus State) that costs her 44.4 cents. And her SS payment is reduced 50 cents. Plus she pays 6.4¢ to SS and 1.45¢ to Medicare. All this adds to 102.25¢, leaving her two cents poorer than if she'd never worked at all. And if she has commuting, clothing and lunch expenses she is further in the hole. Jane probably quits.

One suspects this is not accidental: the laws were actually designed to discourage work. Long ago everyone thought young men needed jobs to support their families, so women and older workers should be pushed out of the workforce. If that ever was a wise plan it isn’t anymore. With so many retirees living so long, if they retire completely the burden of their support falls on those young workers with families, and the taxes will crush them. Whatever they thought in the 1950’s, we have to change the law now.

Incidentally, in 1950 nearly 50% of men over 65 worked, and 10% of women . Today less than 20% of men work and still 10% of women, for an average of 15%. Raising this by 10% should not be hard, and if we raised it to 50% there would be 35% more workers, three-and-a half times what I’ve assumed above. We’d be saved three times over and could build Utopia!

Government representatives will say it's not as bad as this. For each dollar of Social Security withheld this year, SS pays you a higher rate in the future, so in the long run you break even. And you do -- on average -- but the long run is 20 or 30 years, and if you die early you never get it. So a man with a bad heart or a family history of dying at 68 will realize he probably won't break even and will act accordingly. And a woman wanting to work this year because she needs the money and needs the money now, will not go to work if she will only get the money in dibs and dabs over several decades. Furthermore, many people do not know about the break-even arrangement and just know they're being robbed now, so they too stop work before they earn enough to trigger the reduction. When it comes to human behavior, the perception may be more important than the reality.

As to the taxation of $1.85 for each dollar earned, apologists will point out that this applies only until all Social Security payments have been taxed. Beyond that the effective tax rates drop back to normal. The high rate is only a hump in the road. True enough, but many people don't want go over the hump and continue; they stop at the point where it starts. Besides, the hump doesn’t end until around $40,000 in earnings, which is all an average worker earns.

Now, everyone agrees the business of withholding Social Security payments today and returning them gradually later is break-even -- it doesn't make the government one penny richer. But it does cost the government billions of dollars because it discourages people from working. So we should abolish it immediately. This is obvious.

As for taxing SS benefits, Congress should look very carefully at whether this tax brings in more money than is lost by discouraging people from working. I suspect it is a net loser. Still, there is a way to compromise: in the calculation of total income (1/2 SS + Other Income) we could exclude earned income but retain unearned income like interest. Thus we wouldn’t penalize poor Jane who has to work, but we’d still tax the benefits of a millionaire living on his dividends.

Reducing the marginal tax rate on older workers from the present insane 103% to the rational 40% suggested by the Laffer Curve would spur millions of people to return to work. Congress should take these steps.

How to Encourage the Older Worker

We should use the carrot and not the stick. No retiree will be forced to return to work. Nor will they be nor need they be. Many older people miss their work. They miss the stimulation, the camaraderie, the feeling of worth and the money. Yes, they enjoy their leisure, their rest and their travel -- even if they are a little bored. What they would like is to return part time, six months or nine months or eleven months a year. Or perhaps six or four or three hours a day, especially as they grow older.

Their knowledge and expertise are at their height, so they are valuable as well. Yet too often employers want only to exploit them with low part-time wages and zero benefits. Or the employer demands a 40-hour week or nothing.

What we need is a pay package with an hourly rate roughly equal to wages plus benefits before retirement, plus a choice of how much time to spend on the job.

I must emphasize that many people would find this ideal, a far more pleasant lifestyle than TV and rocking chairs, with bingo at the Senior Center Friday nights. My grandmother did important secretarial work in her youth, and was proud of her responsibilities and earnings. At seventy five she worked part-time at the counter of a dry cleaner's and when at last they let her go it broke her heart. She felt useless. Some people want to work, not full time but as much as they can.

So everybody prospers from this plan. The Treasury is saved, a worker gets an ideal life style, and, because Jane won't spend all the money on herself, her granddaughter may get help with buying her first house.

But first of all, Congress should fix the triple taxation tangle.

Whether we can actually increase post-retirement employment by 10% no one can say, nor can we calculate the exact number of trillions the government will collect. But every extra worker bolsters our national finances wonderfully. We should recognize what a treasure we have here, and do everything we can to encourage older workers to return.

Every trillion helps.

A Note on the Multiplier Effect: This effect is recognized in standard textbooks and explained, but no one knows what the multiplier should be. I have used seven, and one sees that figure in many places – evidently it was once taught. But somewhere I saw 2.5, and somewhere else 9 and even 12.5. In theory it rises as the savings rate falls. When the savings rate is zero, as it now is in the US, the multiplier goes to infinity, which is absurd. I have used seven, but someone else may have a better number.

A Note on the Time Value of Money: At 4% compound interest, $1 today will grow to $2.66 in twenty five years. So we can say that $2.66 then is worth $1 today. That is, we devalue future dollars to account for interest.

In the calculations above I have assumed the government will pay the interest on the National Debt, which will allow these extra taxes to pay off the principle gradually, without interest effects. This part is valid.

But the SS and Medicare debts are in present-value dollars, and I have not devalued the taxes over 50 years as I technically should have, largely because I don’t know what interest rate to use. On the other hand, I have assumed Bill will earn $40,000 per year forever, and this is not true either. In fact his wages will rise with productivity. The two effects cancel if productivity-rise equals interest, as it has recently. But nobody knows what either rate will be in the future, so the numbers are not precise and the present value of the future taxes could be more or less than I have shown. Either way, the value of the taxes received will be gigantic and the government should encourage this trend in every way it can.

A Note on Helping Fat Cats

The rich are not hurt by this. A prosperous lawyer will not bother to take SS at 62 – he’s still working , doesn’t need it, and is content to wait till he’s 66 or 70. Besides, he’s earning hundreds of thousands of dollars and high marginal rates on the first forty thousand or so are just a bump in the road to him. The people you hurt here are those earning $13,000 to $45,000, the man who must earn some money for a son’s operation, the lady who’s daughter was laid off and needs some help, the plain folk who need the money and need it now. For them the bump in the road is a giant wall and they’ll never earn enough to pass it. The law is not grabbing taxes from Donald Trump, it’s ruining the lives of the salt of the earth.

Can it Really be This Bad?

The following taxes were calculated with the H&R Block Taxcut program and checked by a CPA. This is the only way to prove how high the marginal rate is – the part of an SS dollar that can be taxed varies from 50 to 85 cents, and State and Federal taxes interact in strange ways (Each is deductible from the taxable income of the other.) All one can do is calculate the tax both ways – with and without an added $1000 of income – and see what happens. That is what has been done here.

Joe, 63, is an Oregonian (highest personal income tax rate in America.) He gets $14,000 a year from Social Security and $20,000 in pension or investment income, and has earned $13,000 so far this year. At $11.50/hour this has taken him six months' work, and he wonders how much better off he'll be if he works another two weeks and makes $1000 more. He knows he may face taxation of part of the Social Security payments, plus a reduction of those payments plus all the regular taxes he loves so well. He asks an accountant.

If Joe earns over $12,480, for each additional dollar of earnings 50¢ is deducted from his SS payments. He has already reached this point, so this will apply to future earnings. If his income, calculated as one half his SS plus everything else, exceeds $25,000, then each additional dollar earned causes 50¢ to 85¢ of a Social Security dollar to be taxed. Joe is at this point too ($7000 + $20,000 + $13,000 = $40,000) If Joe stops now he will keep all his SS and owe just $8076 in all taxes, leaving him with $14,000 SS+20,000 Pension +13,000 Wages – 8076 Taxes = $38,924.

If he stubbornly keeps working and makes $1,000, he loses $500 in SS payments and his taxes shoot up to $8609. His income will be $13,500 SS, $14,000 Earnings and $20,000 Pension

-$8609 Taxes = $38,891, $33 less than he had before. His effective tax rate is 103.3%. Laffer should be crying.

Joe also has commuting expenses. At 20 miles each way for ten days worked (400 mi.), at the government estimated cost of 58.5¢/mile, commuting has cost him $234. At $3 per day for lunches he's paid $30. For total expenses of $264. So instead of being just $33 poorer he is $297 poorer. This is discouraging.

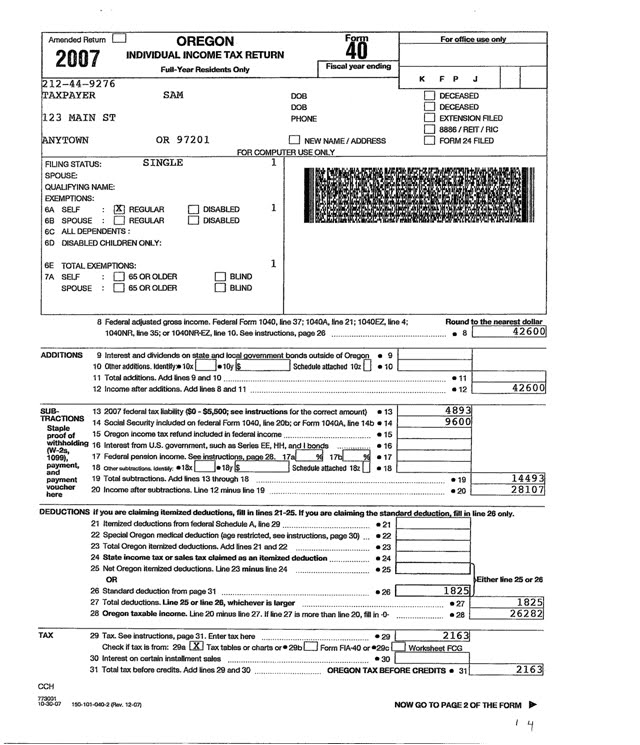

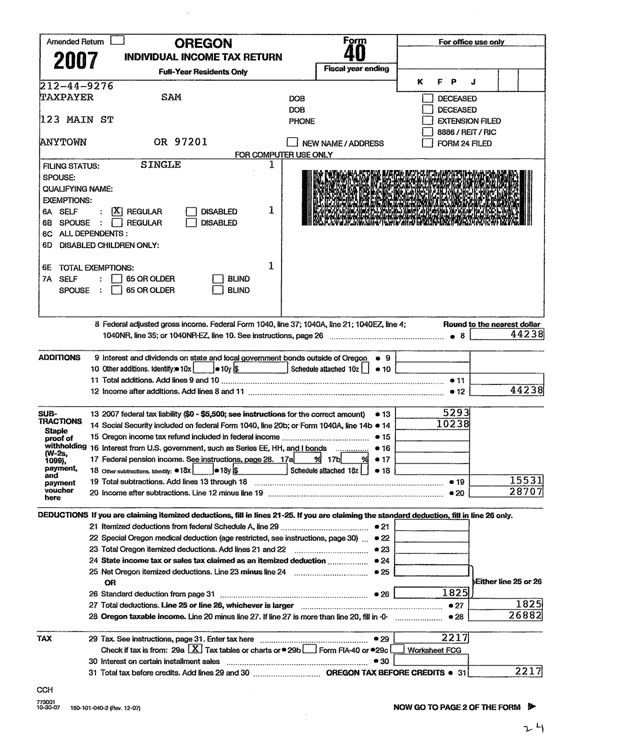

Actual Calculations

{kind=link}

No comments:

Post a Comment